Mannatech Stock: Small But Mighty Health Food Pick (NASDAQ:MTEX)

Everyday better to do everything you love/iStock via Getty Images")

Mannatech (NASDAQ:MTEX) is a health food and supplement maker, direct marketing through distributors and sales associates, with a website for members and the public at large. It’s been in business since 1993, headquartered in Texas. It sells patented and unique wellness and nutritional products all over the world to health-conscious consumers.

A wonderful job of financial engineering since 2017 has leveraged an uptick in profitability at the company during the pandemic. In addition to improving operating performance, management seems laser-focused on returning extra income and cash flow to shareholders with buybacks and dividends. The end result has been above-average margins and returns vs. peers, far superior cash distributions to shareholders, and a double in the stock quote during 2021.

Highlighting a real bargain proposition, Mannatech has generated a 17% free cash flow number over the previous 12 months, on today’s $37 stock price. For a frank real-world comparison, the S&P 500 average company has delivered a free cash flow yield under 4%, less than one-quarter the rate of MTEX.

A big part of the upside story and stronger turn in earnings during 2020-21 can be blamed on the appearance of the COVID-19 pandemic. Consumers are hungry for word-of-mouth food/supplement recommendations to combat the COVID-19 virus, while refocusing on personal health issues. Buying online and shipping to home trends (associates hand out goods generally) help to prop up margins, as no retail location is required. So, the Mannatech business model setup was one ready to take advantage of the new normal COVID economy. On top of these positives, the pandemic has given management an excuse to better align/rationalize costs with sales. Then demand ticked higher. After total sales stagnated for a decade, the 2021 Mannatech has been selling more product with less sales associates and preferred customers.

Mannatech markets a variety of health, wellness, and nutrition products. The company sells a formulated Aloe vera plant extract as its flagship nutritional item. Explained on Mannatech’s website,

Mannatech enjoys an exclusive partnership with Natural Aloe de Costa Rica (NACR), a manufacturer of premium Aloe products in Costa Rica, that cultivates a superior Aloe vera plant. Mannatech and NACR perfected the processes to ensure Manapol contains the most potent form of Acemannan. Well-known for its arid climate and rich volcanic soil, Costa Rica grows the best Aloe on the planet and the company produces the purest Acemannan known to man.

At Mannatech, science continues to remain at the forefront. We continue investing in scientific studies and testing to substantiate the efficacy of our products. Throughout our history, Mannatech has obtained protection for technology relating to our proprietary formulas by securing more than 140 patents in numerous countries around the world.

Exclusive to Mannatech, Manapol is the only commercially available 100% Aloe product that meets the scientifically approved molecular weight definition of 1-2 million Daltons to be true Acemannan as set forth by Chemical Abstract Service (CAS) and American Medical Association’s United States Adopted Names Council (USAN). While other companies claim their products contain Acemannan, no other product meets the molecular grade definition. Mannatech is the only company in the world with true Acemannan.

Mannatech Website Mannatech Website Mannatech Website

Strong Valuation Characteristics

What’s drawn my attention as an investor during 2021-22 are bullish valuation and superb trading momentum traits. Believe it or not, the valuation story has gotten more interesting (not less), as income and sales per share climb faster and faster.

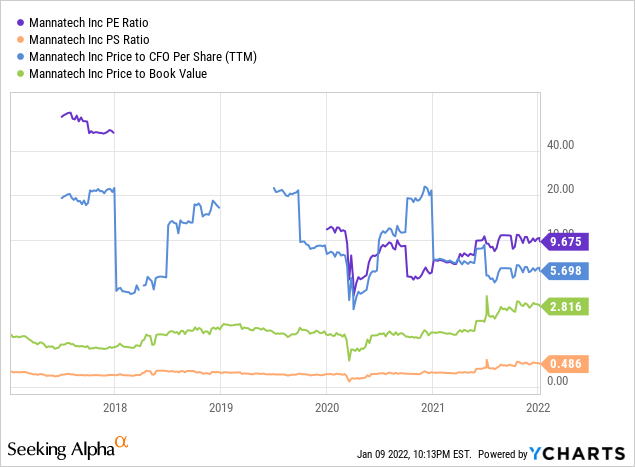

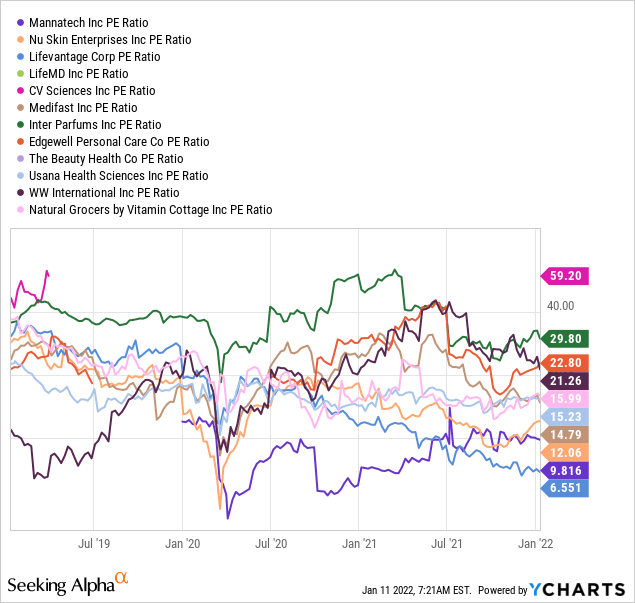

First, we can review some basic fundamental ratios for the company vs. its past 5-year trading history. Price to trailing sales and book value have moved to the high end of the spectrum, just like the vast majority of other U.S. equities. However, in Mannatech’s case price to trailing earnings and cash flow are clearly on the low end of past valuation metrics. Notice pre-COVID the company was struggling to report operating EPS.

YCharts

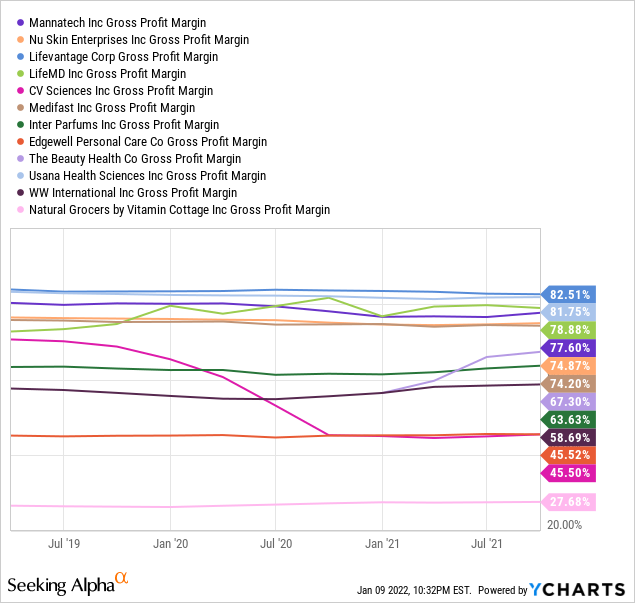

Gross profit margins on sales vs. peers and competitors in the health and nutrition industry are well situated, with a high 77-80% number since 2019. So, if the company can move product to customers in large quantities with an efficient supply chain, alongside low marketing expense, net profits could be sizable.

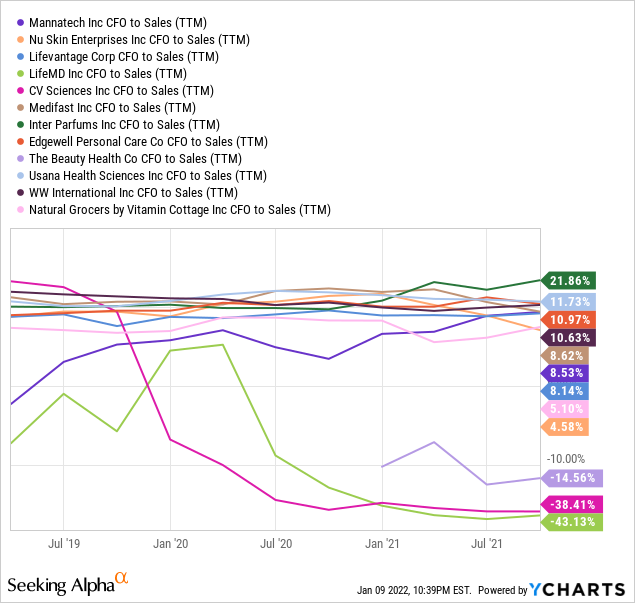

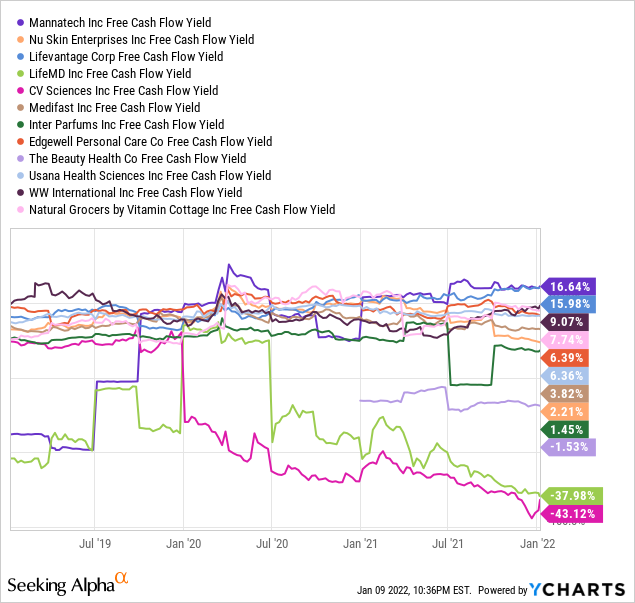

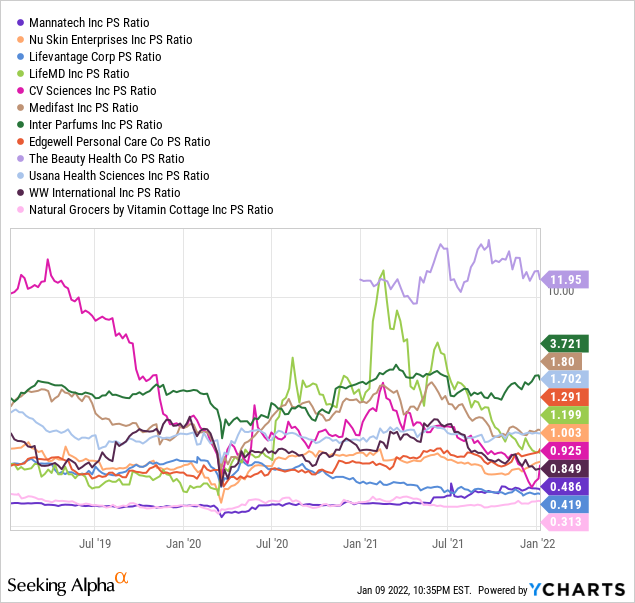

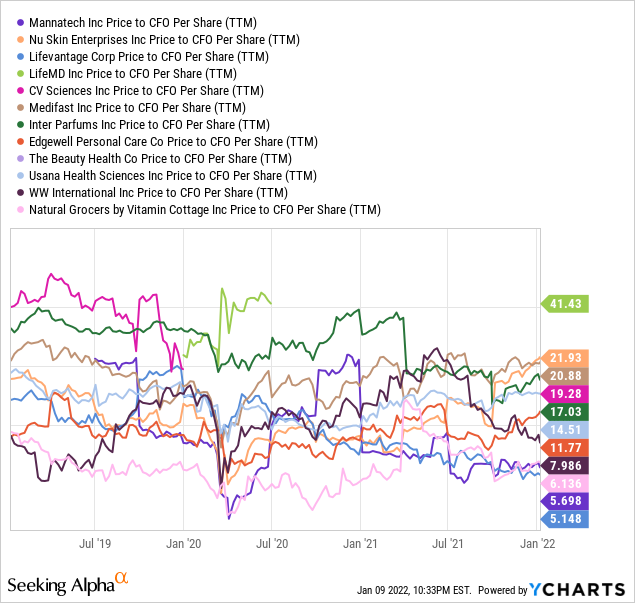

The peer and competitor comparison group includes Nu Skin (NYSE:NUS), LifeVantage (NASDAQ:LFVN), LifeMD (NASDAQ:LFMD), CV Sciences (OTCQB:CVSI), Medifast (NYSE:MED), Inter Parfums (NASDAQ:IPAR), Edgewell Personal Care (NYSE:EPC), The Beauty Health (NASDAQ:SKIN), USANA (NYSE:USNA), Weight Watchers (NASDAQ:WW), and Natural Grocers (NYSE:NGVC).

YCharts

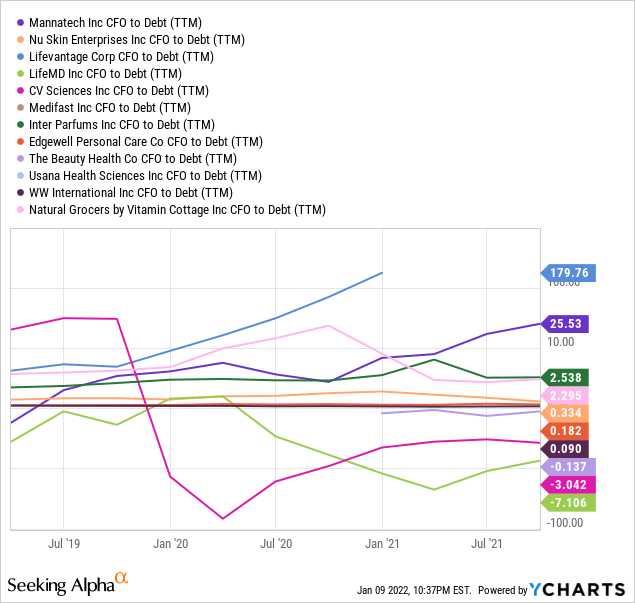

Management has used the spike in cash flow from COVID demand/cost controls to pay off most all debt. Pictured below, cash flow to debt has moved from a negative reading three years ago to a setting where all debt could be paid off with just two weeks of operating cash flow!

YCharts

Keeping debt levels low and operating costs under control, while sales have bumped higher, means cash flow generation is soaring. Below you can see cash flow as a function of sales has moved from one of the worst readings three years ago to a position in the top half of the peer pack.

YCharts

Plus, the company has spent almost nothing on capital expenditures during 2020-21, with CAPEX falling from $2.3 million in 2018 to $700k over the past four quarters. The good news for operations is little CAPEX is required, as 12% of sales are spent on R&D efforts for new supplement inventions, and most all manufacturing is outsourced.

The net result is extra cash flow coming in the door is free and clear of liabilities/IOUs or necessary reinvestment initiatives. Free cash flow available to management has jumped into overdrive. Despite a meaningful jump in the share price from a pandemic low under $7, today’s free cash flow yield at $37 is close to a decade HIGH of roughly 17%! Can rational/conservative investors pass up a low-maintenance and CAPEX spending business, delivering 4x the free cash flow yield of blue-chip choices?

YCharts

Further, Mannatech’s price to sales multiple of 0.5x looks super-cheap vs. the group or prevailing 3x sales ratio for the S&P 500. Price to trailing cash flow per share is bottom of the barrel vs. the health and nutrition group, and one-third the S&P 500 multiple. Price to trailing earnings is next to the lowest of peers around 9x, and a major discount to the blue-chip S&P 500 average around 25x currently.

YCharts YCharts YCharts

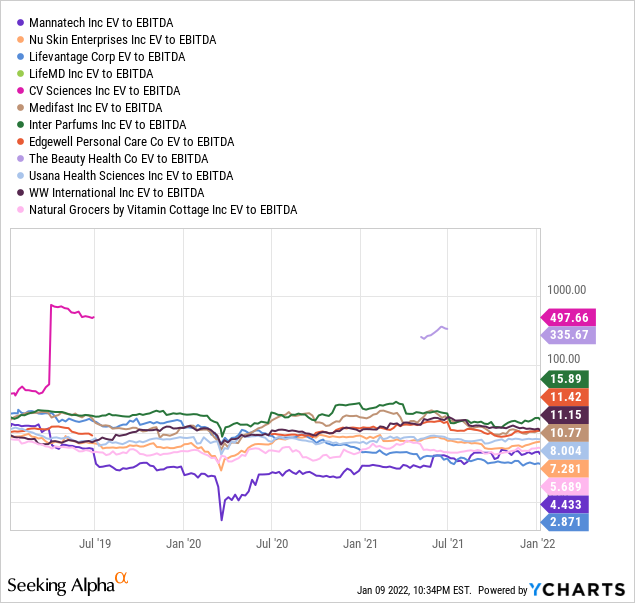

The last data point to ponder, today’s total enterprise value vs. earnings before interest, taxes, depreciation and amortization measurement is running at a 60% discount to the industry median average. In comparison, the S&P 500 EV to EBITDA number is 18x today, well above Mannatech’s 4.4x. If you prefer to invest capital into an efficient and experienced organization, when valuations are lower than you would expect, Mannatech definitely may be worth serious consideration.

YCharts

Insider/Management Confidence

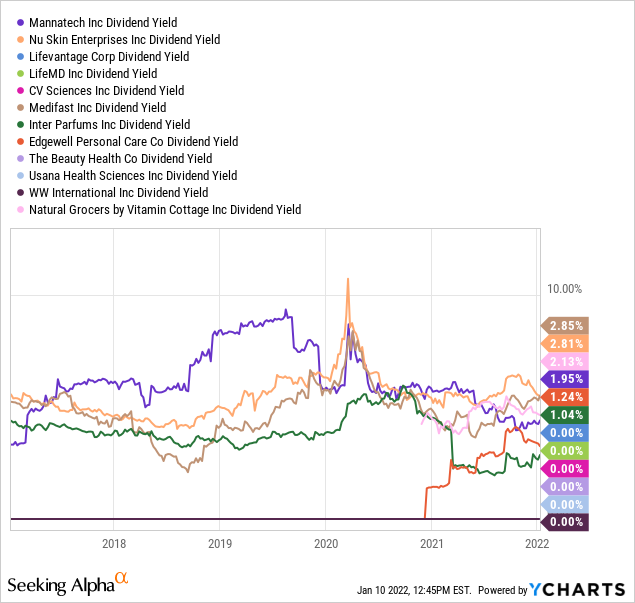

Share buybacks and raised dividends have been the next logical use of extra cash flow and income in 2020-21. The company is in no hurry to buy other assets or increase production rapidly with its cash flow. I count this decision as a huge positive for shareholders. Management raised the regular quarterly dividend to $0.20 last year and even paid a special $1.50 dividend in December. Below is a 5-year graph of the regular dividend payout, expressed as an annual trailing yield on price vs. competitors and peers.

YCharts

Share buybacks have drastically reduced the number of shares outstanding over five years from 2.7 million to 2.0 million today, boxed in red below. The effect of this return of investor capital has been to “leverage” the upside of remaining owners, without using debt.

Seeking Alpha

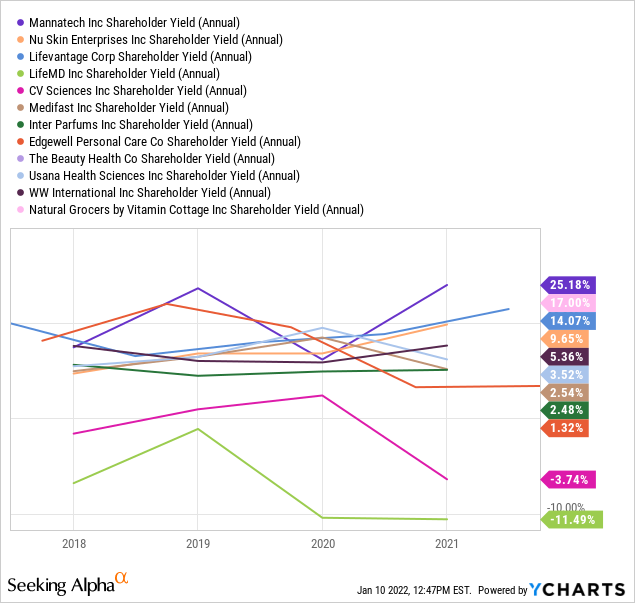

But here’s the kicker. When you include all dividends paid, the major share repurchases, and the elimination of existing debts, Mannatech stands out as the clear winner for Shareholder Yield. Pictured below, we can review the amazing and excellent 25% annual rate of theoretical capital returned to shareholders in calendar 2020, and 15% average annual return of capital on the prevailing stock quote since 2018. More good news, the 2021 number will likely be in the 15%+ zone again.

YCharts

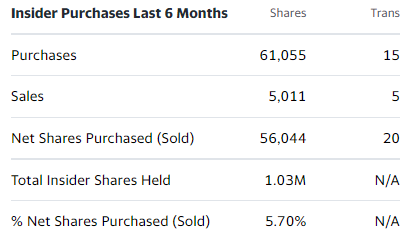

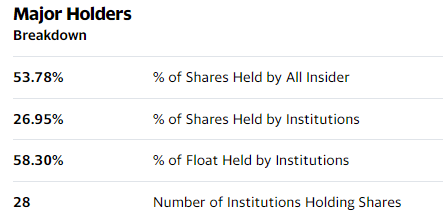

You would think, if upside in Mannatech was nearing the end of this economic cycle, insiders and management would know it, and be selling en masse. Yet, those in tune with the day-to-day workings of the business are increasing ownership through stock grants, while limiting sell volumes. Below are tables highlighting the 53.8% vested interest in the business held by management and insiders.

Yahoo! Finance Yahoo! Finance

Technical Momentum

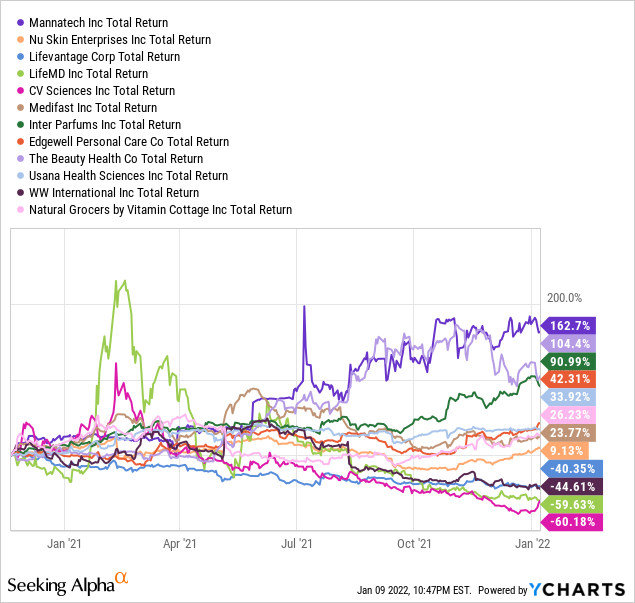

Mannatech has been the leading total return choice for investors in the health and nutrition peer group since November 2020, pictured below. Its 162% advance has occurred through a combination of share quote gains and cash dividends paid.

YCharts

I am modeling nicely positive returns for investors will continue in 2022. Why? The technical chart pattern and momentum indicators I track are still screaming buy. Below is a 24-month chart of daily price and volume trading action. If past is prologue, the low Average Directional Index scores of December-January, like other instances circled in green, may prove a resting stop before another leg higher in price.

On top of this bullish ADX development, the Negative Volume Index’s straight up spike since November may be telegraphing a shortage of supply again. Boxed in red, strong NVI readings often indicate more buyers than sellers on slower news, low volume days. I love this technical condition, if it fits other bullish ideas.

Lastly, On Balance Volume trends have been super-positive during 2020-21, marked with the blue arrow. All told, the powerful OBV rise is signaling strong investor interest over time. Of course, regular share repurchases by the company itself are helping this trend along.

StockCharts.com

Final Thoughts

Mannatech is a prime example of how an uptick in operations can be leveraged for big investor gains, using intelligent financial engineering action. What is a logical price target for the stock in 12-18 months? If net income continues at the current $8 million annual rate on $160 million in total revenue, riding further stock repurchases, and putting a still discounted 15x P/E multiple on EPS gets you to $55 or even $60.

What could go wrong? Two risks stand out to me. Foremost is sales slip and management has to slash prices to move product. Such would degrade cash flow and income, restraining the stock quote. Total sales have not grown much over the last decade, before share buybacks are considered in per share results. In particular, I expect MTEX’s stock trading future to be more dependent and sensitive to total sales growth in 2022 vs. the typical U.S. equity investment.

If you believe like I do, consumers globally will remain focused on healthier diets after the pandemic fades, the odds of a major drop in demand in 2022-23 remain low. And, assuming the COVID-19 economy is our new normal for several more years, Mannatech’s direct selling model should remain quite profitable like 2021.

A second, and more likely risk on your MTEX investment is the U.S. equity market succumbs to a wave of selling in a crash or prolonged bear market scenario. Under this bummer forecast, Mannatech might be stuck in the $30 to $40 range most of 2022.

For a sell-stop level to contemplate exiting a long position (loss prevention on a short-term trade angle), I am looking at the low trades of November-December in the $31 area or the 200-day moving average now standing at $29.

I owned shares on and off again during 2021, and currently hold a small position. I suggest individual investors only put a minor weighting of MTEX in portfolio construction, simply from its micro-cap size. With an equity capitalization around $74 million, regular outside investors will be the last to know if a bearish development finds the operating business.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.