3 angles to pursue when covering medical debt

Last Monday, the White House announced four steps to ease the burden of medical debt on health care consumers. The announcement didn’t get much coverage, and one online publication labeled the White House’s actions a Band-Aid.

That characterization seems harsh because, taken together, the steps Vice President Kamala Harris announced are as follows:

- Hold medical providers and debt collectors accountable for harmful practices.

- Reduce the role medical debt plays in determining whether Americans can access credit.

- Help more than 500,000 low-income veterans get their medical debt forgiven.

- Inform consumers of their rights.

Source: Medical Debt Burden in the United States, Consumer Financial Protection Bureau, February 2022.

It could be that the news fell somewhat flat because the announcement followed the federal Consumer Financial Protection Bureau (CFPB) report last month, “Medical debt burden in the United States.” After that report was published, the nation’s three largest credit-reporting agencies made significant changes in how they report medical debt. We covered those news stories in a blog post last week, “Equifax, Experian, TransUnion to remove some medical debt from credit reports.”

When reporting on medical debt and the White House announcement, it’s easy to neglect three of the most compelling angles to this story, all of which stem from the abnormal nature of the highly complex U.S. health care system.

First, the nation’s credit reporting system adds a burden to those who cannot afford to pay their medical bills that high-income consumers do not face.

Second, the health care system can be financially toxic to patients because after addressing one’s physical illness, hospitals, health systems, physicians and other providers burden the poor and disadvantaged with medical debt that leads to depression, anxiety and suicide, as the CFPB reported. Also, as Harris noted, medical debt can have negative health effects because, referencing a recent study, almost half of people with medical debt have avoided seeking care. In September, the National Bureau of Economic Research published that study ahead of print, “The Impact of Financial Assistance Programs on Health Care Utilization.” It’s scheduled for publication in September in the American Economic Review: Insights.

Third, most Americans are unaware that medical debt is rare in other industrialized nations.

On the first issue, the White House was addressing the credit-reporting burden in significant ways, according to Wesley Yin, Ph.D., one of the researchers on the NBER report.

In a recent interview, Yin told AHCJ the White House announcement is important for many reasons, particularly because the federal Department of Health and Human Services (HHS) would begin holding some hospitals, health systems, physician organizations and other providers accountable for their actions when consumers cannot pay their medical bills.

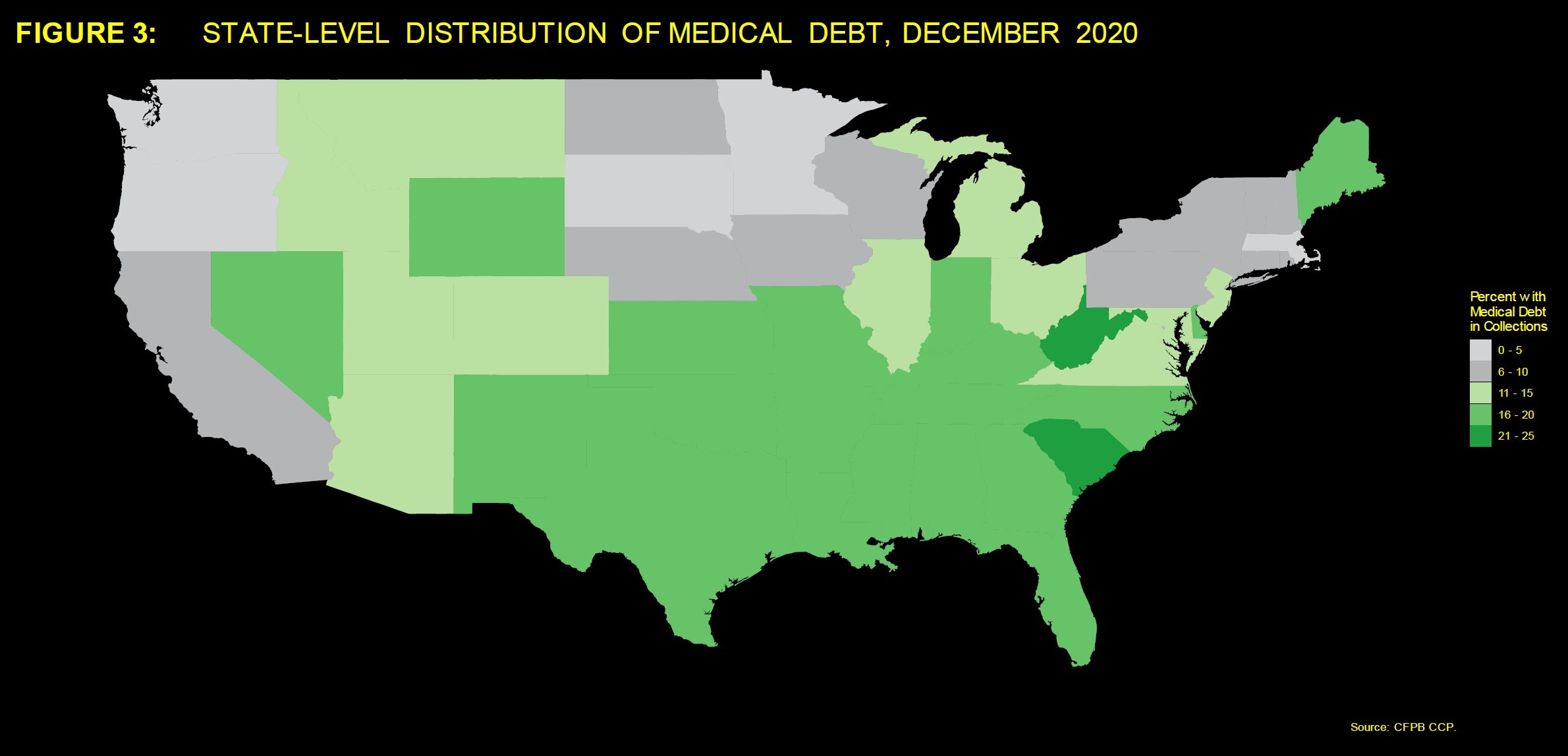

Source: Medical Debt Burden in the United States, Consumer Financial Protection Bureau, February 2022. Map shows the share of individuals living in each state who have medical debt in collections as of December 2020.

The data collection and monitoring the White House is asking HHS to do could have an immediate sentinel effect on how providers behave toward consumers who cannot pay for their care, says Yin, an associate professor of public policy at the University of California Los Angeles.

“Just shining a light on that type of behavior might lead to reducing the most egregious practices from providers,” he noted. Some hospitals and health systems have filed lawsuits against patients who should have qualified for financial assistance programs that those hospitals and health systems are supposed to offer when consumers cannot afford their care, he adds.

See, for example, this article from Health Affairs in December, “Hospital Lawsuits Over Unpaid Bills Increased By 37 Percent In Wisconsin From 2001 To 2018.” Also, check out this tip sheet about the excellent work from Jay Hancock and Elizabeth Lucas at Kaiser Health News, “Pulitzer finalists outline tips for covering abusive hospital billing and collection practices.”

Many health care systems and other providers report that they offer charity care as part of their mission. “But in practice, enrollment in financial assistance programs may not be easy or encouraged,” Yin says. “That’s why the White House’s actions to shine a light on charity care practices might have a positive effect for low-income individuals, and nudge providers to be stronger advocates for increased subsidies for health insurance and Medicaid expansion.”

Last year, Yin was one of the authors of a research report in JAMA Network, “Medical Debt in the US, 2009-2020.” In that study, researchers found medical debt was highest in the South in low-income areas and was concentrated in lower-income communities in the 12 states that have yet to expand enrollment in Medicaid.

The researchers also showed that medical debt totaled at least $140 billion and has become the single largest source of consumer debt, adding up to more than all other sources of consumer debt combined, Yin says.

The U.S. health system is an outlier

The second angle to pursue is how much U.S. consumers pay out of pocket for medical care, even if they have insurance, as Noam N. Levey reported in a series of articles for The Los Angeles Times in 2019.

The third angle to cover is how the U.S. health care system ranks last among high-income nations in access to care, administrative efficiency, equity and health care outcomes despite spending much more of our gross domestic product on health care. Last summer, this blog covered this topic and reported on Levey’s excellent series.

Regardless of whether other countries have government-run health care or use commercial health insurers, almost all of America’s global competitors strictly limit out-of-pocket costs, wrote Levey who joined Kaiser Health News in January 2021.

The burden of medical debt is so extreme in the United States that it often leads to bankruptcy, another crushing financial blow that is rare in other nations, according to this report, “Medical Bankruptcies by Country 2022,” from the independent, nonpartisan World Population Review. Bankruptcy because of medical debt is rare in other nations because most other developed economies (except China) have single-payer health care systems that use taxes to pay for medical costs not health insurance policies that individuals and families buy, the report showed.

In the CFPB report, agency Director Rohit Chopra said consumers should be free from what he called a “doom loop” resulting from medical bills.

“Even when a patient tries to battle to get an accurate bill or an insurance claim paid, medical debt collectors have a weapon that is hard to fight against: the credit report,” Chopra said. “I am concerned that the credit reporting system is being weaponized as a tool of coercion to get people to pay medical bills they may not even owe.”

Chopra also questioned whether medical debt can be considered “real debt,” as it falls outside the norms for routine business transactions.

“Few people choose to take on medical debt, and typically, patients have no idea how much they will be charged for a service or a procedure. There’s no upfront disclosure or interest rate to compare,” Chopra said. “Individuals and families must confront a billing and collections system that can be best described as error-plagued, confusing and labyrinthine.”

After the CFPB issued its report, Equifax, Experian and TransUnion said they would remove some medical debt from credit reports. For The New York Times, Tara Siegel Bernard reported on March 18 that the three companies would remove negative marks for consumers who settled a debt after it went to collections.

Consumer advocates cheered the changes saying they reflected the idea that such debt is not the best predictor of a consumer’s financial behavior, she wrote. Bernard quoted Chi Chi Wu, a staff attorney at the National Consumer Law Center, saying the changes will help people whose medical debt stems from owing insurance copayments and deductibles, which usually fall under $500.

But these changes won’t do much for “the scores of people with the largest unpaid debts, who are often dealing with catastrophic or costly illnesses that result in high bills even with insurance coverage,” Bernard wrote. These consumers are the sickest, poorest and most vulnerable, Wu told her.

As we might expect, medical debt in collections is common among people of color and among the poor, veterans, seniors and young adults of all races and ethnicities, the report showed. Note that Harris highlighted the work of the federal Department of Veteran Affairs to end reporting of medical debt for veterans with bills from the Veterans Administration.

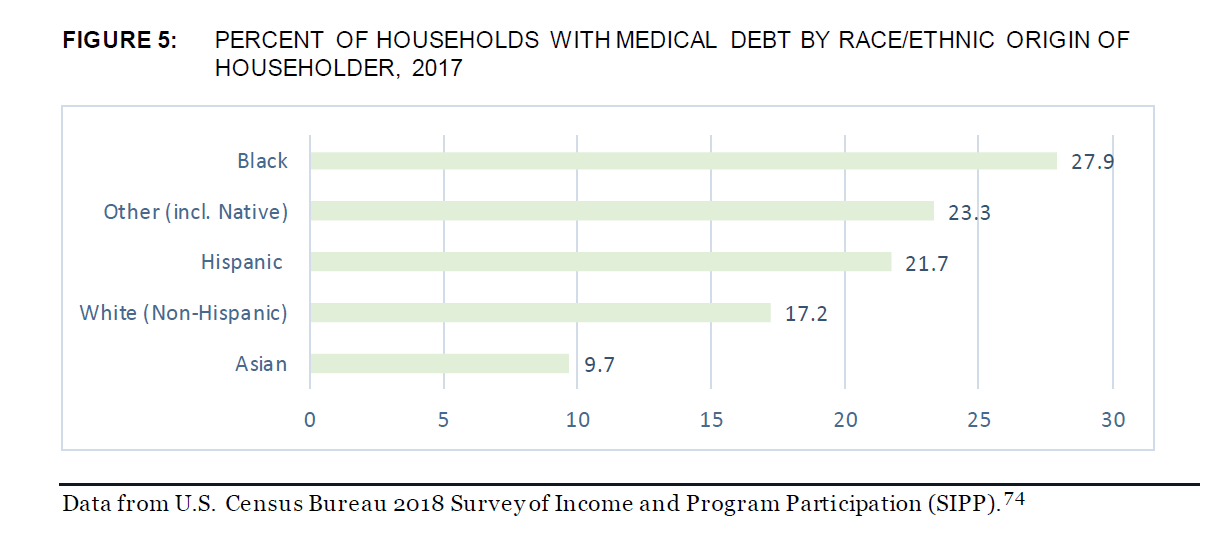

Citing a 2018 Census Bureau survey, the CFPB reported that among Black households, 28% had medical debt; followed by Hispanic households, 22%; white households, 17%; and Asian households, 9.7%. The report also showed medical debt in 23.3% of households in other racial and ethnic groups, including Native American and Alaska Natives.

A good place to start your reporting on the “doom loop” often seen with medical costs is Marshall Allen’s book, “Never Pay the First Bill.” Allen calls it “the guerilla guide to health care the American people and employers need.” AHCJ offered highlights of Allen’s book in a July 2021 article and interviewed Allen a length in an October webcast, where the author outlines the steps journalists and patients can follow to push back.

Additional resources